Why Obamacare Will Never Work to Save Money

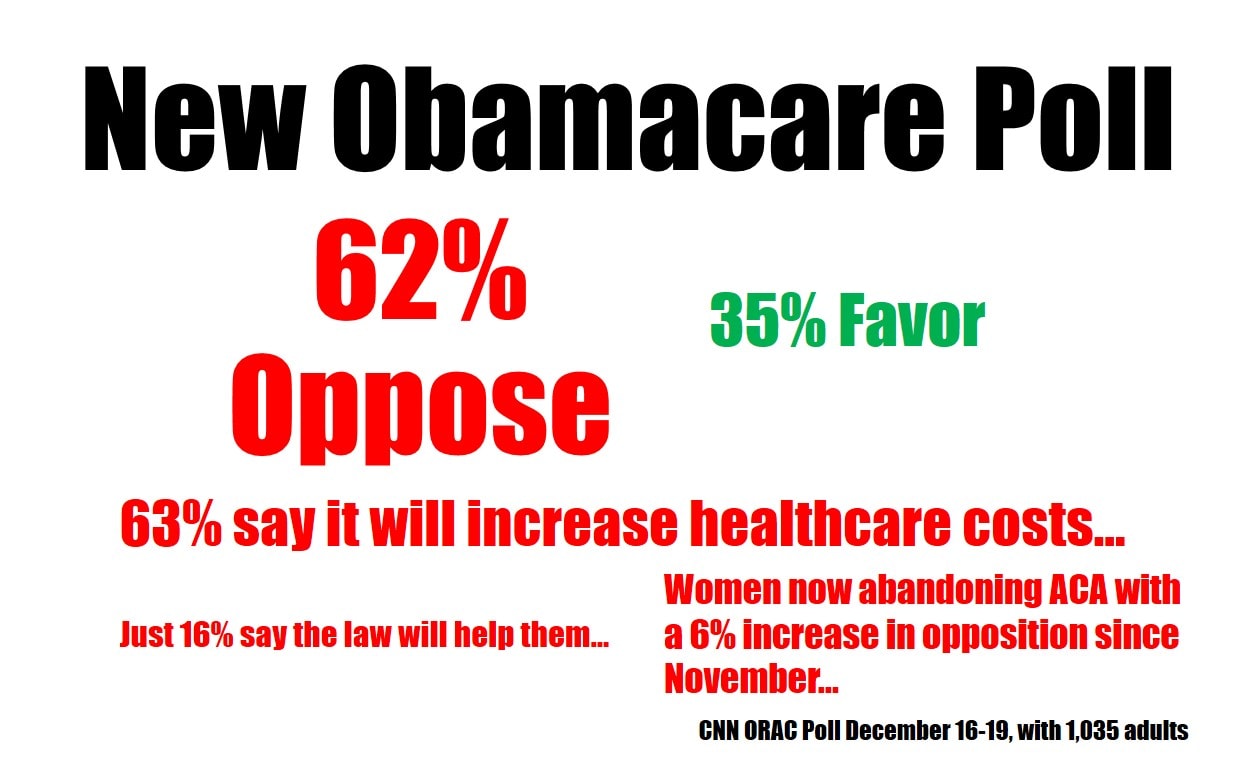

Do you have any idea why Obamacare will never work to save money? A new poll out yesterday paints a grim picture of the public’s perception of Obamacare (see above for summary). Regardless of your political bent or your love or hate for the president – it highlights what people are now just recognizing – Obamacare is a deeply flawed attempt at controlling healthcare costs. Basically the elephant which is modern US healthcare desperately needed a diet to help it shed unwanted pounds, instead we just gave it an all you can eat Vegas buffet. Let me explain.

Why Healthcare Costs So Darn Much…

American medicine’s healthcare cost problem began in WWII. At the time, because of wage controls, employers needed something to attract new workers that they could offer the scant work force . The concept of health insurance was born as an employee benefit. This erased the concepts of pricing, supply, and demand because a third party began paying for healthcare.

To better understand why costs have soared, I need an example. The one that always seems to work best for my patients is consumer electronics. For instance, what if I told you that your employer would give you a benefit that would allow you to buy whatever you wanted at Bestbuy for a $25 co-pay? Would you buy the modest flat screen you were planning on buying on sale, or would you buy the biggest and best TV they had-maybe the new 80 inch 4K ultra-high def that retails for $25,000? Human nature dictates that you would get the biggest one they had. In addition, Bestbuy managers would soon notice that the third parties paying the bills were paying for these bigger TVs and would start raising prices and stocking only the big and expensive sets. After all, who would want small and unimpressive TVs when the big ones were essentially free to the consumer?

Enter Obamacare into Our TV Analogy

Let’s say our TV buying analogy runs it’s logical course and you can no longer buy a nice TV set for under $100,000. Most people have no issues with getting a new TV as they have employer sponsored TV insurance. Some people in the market purchase their own TV insurance, but to make it affordable, it’s a catastrophic policy, so if their set at home dies, they can afford the $50,000 bare bones TV with a big, but manageable $2,500 co-pay. However, the people without employer sponsored TV insurance or those too poor to buy coverage would go bankrupt just trying to buy a new TV, so we create a government program to make sure that everyone is covered. Since we require everyone to have this new TV insurance, there’s a bit of a free for all as the law is crafted. After all, the TV insurance guys have powerful lobbies by now as does Bestbuy. So the TV insurance lobby throws a hissy fit and says that for it to buy into this new plan people who buy these new government policies must buy more TV than they actually need. Eventually, the Mastodon sized program created by a committee of lobbyists, mandates that TV insurance must cover only the new 80 inch models with Bose surround systems and built-in stadium seating. What’s not to like about this new plan, right? The people who can’t afford TV insurance get it paid for by the government and TV insurers and Bestbuy can force you to buy the biggest and best set they sell.

Our TV insurance program (now loving called “BestbuyCare”) comes with a hidden issue (although not so hidden to anyone who bothered to take a college econ course). In order for the TV insurers to sell you more TV than you need, they have to dramatically increase the cost of TV insurance. So what used to run two hundred dollars a month jumps to $600 a month. However, our government program has a solution! It will appoint TV experts on massive, government picked panels who will meet regularly to control the costs of new TVs. There’s just one catch, half of the experts on the new panels are on the Bestbuy payroll, own Bestbuy stock, or work or do paid research for the TV manufacturers or parts suppliers. So much for cost control!

Moving From TVs to Healthcare

For some my TV analogy may have been uncomfortable, after all we’re talking about lives here and not something as silly and overall meaningless as a new TV. So let’s switch back to healthcare and why Obamacare in particular can never work.

Forgetting about the enrollment issues and that the US government just blew a billion of your hard earned dollars on a barely functional web-site, let’s look at a core feature of the ACA-government mandated minimum coverages. President Obama (disclosure-who I voted for in 2008) campaigned on a few key talking points about Obamacare. If you recall, one of these was an attack on so called, Cadillac plans (insurance plans that covered too much). This past two months we found out that Obamacare doesn’t like Cadiilac plans because they have been replaced with Rolls Royce plans.

Let me give you a concrete example. Several female patients over age 55, whose old insurance plans didn’t have the required coverage, have relayed that they were required by the exchanges to buy maternity coverage (I call this the “immaculate conception rider”). In addition, these new plans must now cover drug rehab, something few plans had in the past. In fact, the required coverage list looks like a who’s who in healthcare lobbyists-each got a coverage mandate for their employers. So regardless of how much Obamacare can save us, it’s starting by offering the healthcare elephant a smorgasbord and then relying on will power to do the heavy lifting of shedding healthcare cost pounds.

All is not lost! There is a major cost containment system baked into these new Rolls Royce policies: the IPAB. This stands for Independent Payment Advisory Board. The IPAB will control costs by deciding which care gets covered by Obamacare and which doesn’t get covered. As you might imagine, like our TV example above, if you’re a drug company selling an expensive drug, you have been working night and day to get your bought and paid for university guys on these panels. In fact, as most of the public knows, the concept of an “Independent” government panel is beyond an oxymoron. For better or worse, our form of representative government has evolved to give the folks with the biggest checkbooks the most representation and the IPABs will be no different. Hence, if anything, the IPABs will increase and not decrease costs-it’s just the nature of the Pharma beast.

Wait! There’s another cost saving mechanism-medical homes. The concept is that the American hospital and it’s tentacles in the community will become the nexus for a cost savings revolution. However, the American hospital is the least efficient and most expensive cost savings mechanism ever devised by man as it grew up in a world of unlimited funds that didn’t rely on the rules of supply and demand. Conceptually, this is a bit like placing Bestbuy at the heart of the new government TV program-“conflict of interest” is too soft a term.

Wait, there’s a final fail safe government cost saving mechanism, “capitation”. Obamacare has recycled this failed cost savings measure from the 1980s, slapped some lipstick on that pig and renamed it as part of the medical home. This means that instead of paying your doctor for every time he sees you or does a procedure, Obamacare will encourage doctors to accept lump sum payments for a patient’s total care needs. While at first blush this looks like it might actually work, it crashed and burned in the 80s because doctors began rationing care to make more money (the less your doctor spends on you the more he can keep). This care rationing actually drove up costs as instead of treating small problems early, the doctors let those problems become bigger and more expensive before they would cut into their capitation bonuses. In addition, patient complaints to state insurance commissions soared, as it didn’t take patients long to figure out why the doctor was saying no.

While there are other parts of the Obamacare cost savings plan that are destined to fail; mandated coverage, medical homes, and capitation are the big three. However, there’s another issue looming that will blow up the whole plan. The insurers are now revolting.

While most insurers looked at Obamacare as a cash cow that would force consumers to not only buy their products, but buy way more of their products than they needed (and give government subsidies to those who couldn’t afford these purchases), all of this only works from an actuarial standpoint if one thing happens-everybody is forced to buy insurance. While you’ve heard of the more obvious issue of Obamacare needing the young and healthy to sign up, there’s also another issue afoot.

First, for Obamacare to work, you need young and healthy people who don’t normally buy or use insurance to sign up. However, my young patients have shown me why this will never work by bifurcating into two groups-those that need coverage and those that could care less. For those that need coverage because they have a medical problem, they have gone from cheap high deductible plans costing $100-200 a month to required Rolls Royce plans at $500 a month. Those who can’t afford the crazy fees are told they must now become wards of the state and join Medicaid programs. The only issue is that locally, there are few providers who take Medicaid. The other group of young adults will just take the $9 a month IRS penalty (if they ever get caught) rather than pay $500 a month for a Rolls Royce plan they neither need nor want. In addition, without pre-existing conditions, if they do get sick, it’s cheaper to but a Rolls Royce policy when that happens and not waste money that could be going towards a new iPhone on something as abstract as healthcare insurance.

The second issue is an even bigger problem than the first, as it’s alienating insurers. The Obama administration’s way to deal with the crazy high cost of the Rolls Royce plans is to delay the deadline for buying one. This past week it told the 6 million Americans that have to buy new policies on the exchanges that they could keep their existing plans for another year. In addition, it handed a huge Christmas present to the Unions, by creatively interpreting it’s own rules that self-insureds (like Unions) don’t have to comply with the mandate. In the meantime, insurers are now worrying that the rich spreadsheets they counted on to prop up this whole inflated mess are now not workable-i.e. these political decisions will undermine the actuarial basis so that they are unable to make money.

Wrapping It All Up for Christmas

So is there a way to fix this mess? Yes. Going back to our Bestbuy example, the fix is simple. Force consumers to get skin in the game through health savings accounts, which will deflate the medical pricing by re-installing supply and demand in healthcare. If a consumer knows that the money he or she pays for that “80 inch TV” will impact their pocket book in some substantial way, they’ll start to pay attention to prices and will eventually opt for the 42 inch model they need, rather than the 80 inch model they want. In the meantime, there’s nothing about Obamacare that solves that problem. So expect higher un-affordable healthcare prices courtesy of the Affordable Care Act.

NOTE: This blog post provides general information to help the reader better understand regenerative medicine, musculoskeletal health, and related subjects. All content provided in this blog, website, or any linked materials, including text, graphics, images, patient profiles, outcomes, and information, are not intended and should not be considered or used as a substitute for medical advice, diagnosis, or treatment. Please always consult with a professional and certified healthcare provider to discuss if a treatment is right for you.